Chugai has ample net cash (cash and cash equivalents plus marketable securities less interest-bearing debt) amounting to roughly half of annual revenues. At the same time, we will generate cash flow with steady earnings each year. Cash management will be a priority, and our policy in IBI 18 is to allocate those funds to invest proactively for the future and to provide appropriate returns to shareholders.

In making investments, we will continue to practice sound cash management while implementing the strategies I outlined above. For example, in the recent site acquisition and the subsequent facility construction, which are major investments, the handover of the site will be completed at the end of 2018 and construction will start in 2019. This means investment in the structures will begin, but we will maintain cash on hand at the current level to make further investments for the future, and we estimate that we can cover that investment with the current cash flow level.

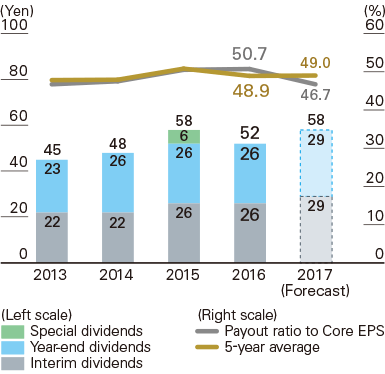

Based on the idea that Core basis* net income should be divided evenly between the Company and its shareholders, we set the target for the payout ratio at 50 percent of Core earnings per share (EPS) on average. This approach has been commended by shareholders and investors for its clarity, but at the same time, it sends a message that our common standard for establishing the Company’s targets and returns to shareholders is Core basis profit growth.

We also receive questions about capital cost and ROE. Naturally, we understand that ROE needs to be greater than the cost of capital. Internally, we calculate and analyze the contribution margin of each product based on the cost of capital, and the results are shared among management. However, what I would like investors to understand is that we place importance on aligning externally disclosed targets with internal Company-wide targets and on the clarity of target-setting, and for these and other reasons we use simple Core basis operating income for financial targets.

I have sensed changes for the better among institutional investors in Japan since the announcement of Japan’s Stewardship Code. On the other hand, I feel that this could become a case of “once bitten, twice shy,” and it should not lead to a situation where dialogue is not encouraged.

Chugai's basic strategy is to continuously generate profits and increase its corporate value through innovation, and then return the results to shareholders through higher valuation in capital markets and stable dividends. Therefore, our IR policy is to share common goals with investors who believe that they and the Company are equal partners, to engage in discussions with them on an equal footing, and to grow the Company so that their investment is a success. That’s the kind of appropriate relationship I hope to build.

We have focused on making the content of Chugai's integrated report (annual report) easy for investors to understand in order to share our management direction and the events behind it. This year, we have designed the report to make it even more user-friendly and convenient. It is always evolving, and we want it to be a starting point for dialogue.

We will continue to do everything we can to communicate and provide disclosure from the standpoint of investors to facilitate a more effective dialogue and meet their expectations.